When accessory dwelling units (ADUs) first began making headlines in 2017, many thought they could be the answer to helping families stay housed in high-cost areas, but with rising construction costs and strict financing requirements, it soon became clear that ADUs were still out of reach for those that probably need them most.

The government is well aware of this issue, which is why we’re thrilled to see policymakers taking action to make financing more accessible for modest-income families.

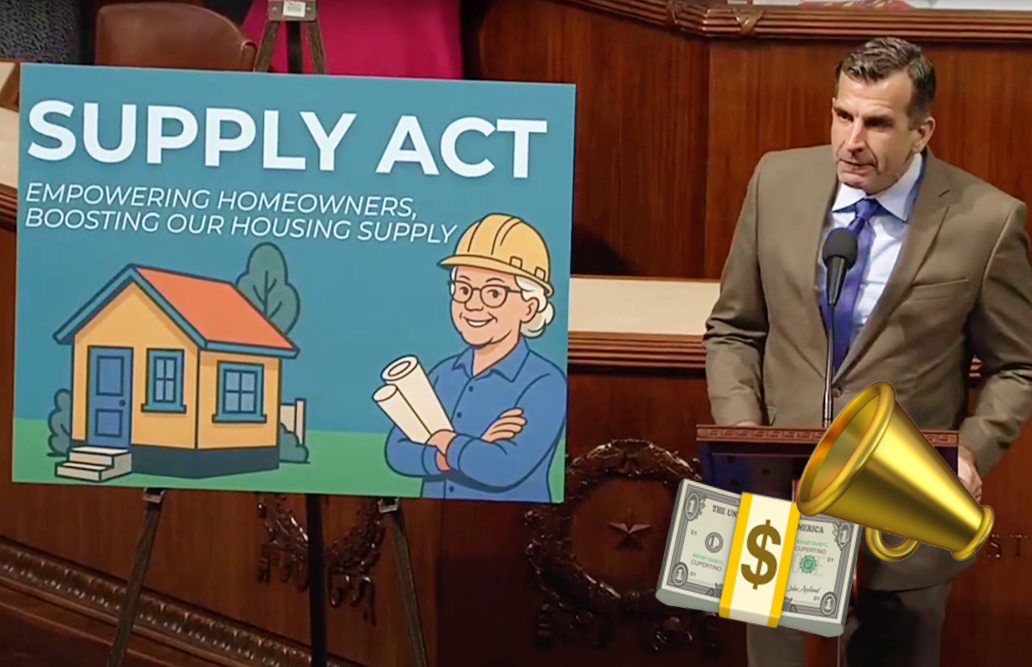

Introducing the Supporting Upgraded Property Projects and Lending for Yards (SUPPLY) Act. Congressman Sam Liccardo (D-CA) and Congressman Andrew Garbarino (R-NY) have drafted a new bill that is designed to offer a practical solution: affordable, government-backed loans specifically for building ADUs. The SUPPLY Act would allow homeowners to access second-position financing, a type of loan that lets them keep their existing low-interest mortgage while securing the additional funds needed to construct an ADU.

You can read the official document here. But, if you’d prefer a (ahem) simpler translation of the jargon-heavy bill, keep on reading.

The Problem with ADU Financing Today

While ADUs are a promising solution to the housing crisis, the path to building one is often blocked by a major hurdle: financing.

Currently, most ADUs are funded through one of three methods:

- Cash savings

- Home Equity Lines of Credit (HELOCs)

- Cash-out refinances

All of these require one thing: significant home equity. That puts them out of reach for many modest-income or first-time homeowners, who may not have built up enough equity, or any at all, to qualify.

You can read more about the various ADU loan options here.

Even those with strong incomes and good credit often hit a wall when they try to secure a second loan to finance their ADU. That’s because traditional lenders see second-position loans as too risky, especially when a first mortgage is already in place.

While there are options for those with low equity like construction loans, these usually come with higher interest rates and stricter requirements than the other options.

Without accessible and flexible financing options, thousands of homeowners are left stuck; wanting to build, but unable to break ground.

This is the problem that the SUPPLY Act aims to solve.

What Is the SUPPLY Act?

The Supporting Upgraded Property Projects and Lending for Yards (SUPPLY) Act is a bipartisan bill aimed at making it easier for everyday homeowners to finance the construction of accessory dwelling units (ADUs).

Introduced by Representative Sam Liccardo (D-CA) and Representative Andrew Garbarino (R-NY), the bill has garnered support across the political spectrum, with endorsements from housing and finance leaders including the Casita Coalition, National Association of Home Builders (NAHB), Mortgage Bankers Association, and the California and Nevada Credit Union Leagues.

At its core, the SUPPLY Act addresses one of the biggest barriers to ADU construction: a lack of accessible and affordable financing. Here’s how the bill proposes to fix that:

HUD-Backed Second-Position Loans

The SUPPLY Act would allow the U.S. Department of Housing and Urban Development (HUD) to insure second-position loans specifically for ADU construction. These loans would sit behind the homeowner’s existing mortgage, making them far more accessible for people who may not have enough equity for a refinance or HELOC.

By having the federal government back these loans, lenders are more likely to say “yes” to homeowners who would otherwise be turned away, especially modest-income families or first-time buyers.

Flexible Financing Specifically for ADUs

Unlike traditional home improvement loans, the financing under the SUPPLY Act would be tailored specifically to ADUs. That means:

- Loan structures that align with typical ADU project costs

- Terms designed to accommodate construction timelines

- Eligibility criteria that account for rental income potential (up to 50%) or multi-generational use

This flexibility makes it possible for a wider range of homeowners to access funds—and get to building faster.

Homeowners Keep Their Low-Interest First Mortgage

One of the most important aspects of the bill is that it preserves the homeowner’s existing mortgage. Instead of requiring a refinance (which can lead to a higher interest rate), the SUPPLY Act enables financing on top of a current mortgage, helping homeowners avoid disrupting their favorable loan terms.

This is especially critical in today’s interest rate environment, where refinancing can mean giving up a sub-4% mortgage in exchange for a much higher rate. The SUPPLY Act solves this problem by keeping the first mortgage intact while still offering the funds needed for ADU construction.

How the SUPPLY Act Could Change the Game

By unlocking new financing options, the SUPPLY Act has the potential to make ADU construction a reality for a much broader range of homeowners. Not just the wealthy few with deep equity.

Here’s who stands to benefit:

- Lower- and middle-income homeowners who need an extra unit for rental income or family support but can’t access traditional loans.

- Younger homeowners who haven’t built up equity but want to invest in their property and grow long-term wealth.

- Multi-generational households looking to care for aging parents or adult children without relying on costly assisted living or rentals.

With second-position, HUD-backed loans, these homeowners would finally have a practical path forward, without sacrificing their existing low-interest mortgage.

The ripple effects could be significant. More ADUs mean more housing supply, which helps stabilize or even reduce rents in high-demand areas. And with more families able to build units in their backyards, we could see thousands of new rental homes created without breaking new ground in open space or disrupting neighborhood character.

What Happens Next?

The SUPPLY Act was introduced in the House of Representatives in July 2025 and is currently awaiting review by the House Financial Services Committee. This is the first major step in the legislative process. For the bill to become law, it must be approved by the committee, then pass votes in both the House and the Senate, and finally be signed by the President.

Given the bipartisan support and endorsements from key housing and finance organizations, there’s momentum. But legislation like this can still take months or even years to move forward, especially if it becomes part of a larger housing package.

If passed, the rollout could take additional time as HUD designs and implements the loan program. Realistically, it may be at least 12–24 months before homeowners begin to see the benefits.

In the meantime, make sure you’re subscribed to our newsletter and download our free ADU Starter Kit to stay up to date with all the latest ADU news. Maxable has a finger on the pulse of new legislation, financing opportunities, and design trends, so you’ll always be one step ahead in your ADU journey.